Thesis Busted - Kitchen Sink Quater

Thesis Busted - Kitchen Sink Quater

CURI released its Q4 2022, which was horrible. I go through the updated thesis, bull and bear case. Disclosure and Disclaimer. This is not investment advice and I own CURI stock.

Q4 2022 Background

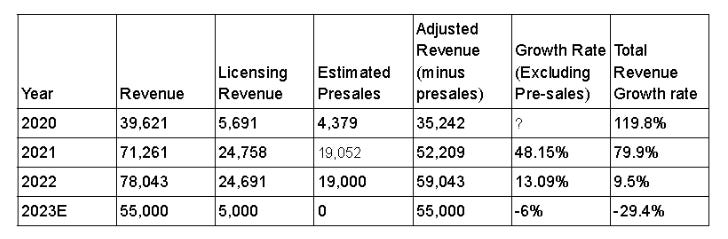

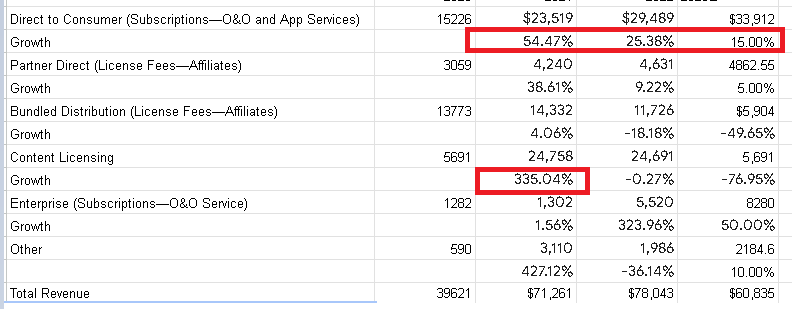

The major news is that Curiosity Stream missed both the top and bottom lines, reporting a significant reduction in revenue in Q4. Zooming in, the leading cause of the drop in revenue is the 9.5M drop in content licensing (From 12.5M Q4 2021 to 3M Q4 2022). This was followed by a decline in bundled distribution. DTC and Enterprise sales increased in the quarter.

According to management, starting from 2023, zero margin pre-sales content licensing revenue, which amounted to approximately $19M in 2022 (content licensing cost in 2022 is 24.5M ), will be in the low-to-mid single-digit million dollar range in 2023.

What is this pre-sale licensing revenue? The management did a HORRIBLE job communicating the mechanics to the general investing public & retail investors. Read more about pre-sales here: https://timtortora.com/pre-sales-what-are-they-and-why-do-they-matter/. It's a funding mechanism where a film producer pre-sells rights (platforms & geographic rights). In theory, this helps build up content libraries. It can partially tap into others’ capital to fund/ acquire films.

However, CURI is no longer trying to increase revenue at all costs but instead reduce cash burn. Therefore, fewer films are produced, resulting in less content licensing revenue. Looking at it from this lens, in a way, this is bullish as management finally dared to take the revenue hit and to investor perception to spend less cash to acquire content.

Furthermore, was some positives:

DTC customer and Enterprise Sales increased (expected)

84% increase in subscription prices. I agree they should charge more for niche power users of the app. I think this would increase revenue. I get a sense that CURI has previously priced their service too cheaply.

Getting out of unprofitable deals, even though gross profitable, which has marketing obligations. The question is, why did they even do this in the first place?

Reduction in G&A cost by 29% QoQ and YoY. This is surprising considering CURI is already lean, with less than 100 employees.

Product updates - Launching in more geographies, price increase and launch of FAST (Free Ad-Supported Streaming Television), AVOD (Advertising-based Video on Demand). New hires for the sponsorship.

Focus on free cash flow - I have previously blogged about the unreliability of using GAAP accounting for Video assets. This is another case of how useless the income statement is for investors.

Implications

Firstly, it is worth mentioning that management mentioned in the Q&A that the license revenue is lumpy and that there is “interest” in the content library. Management is implying there might be optionality in licensing revenue. However, given that content spending in the industry is decreasing and they had half a year (Q4 2022, Q1 2023) to find interested licensees, I’m sceptical that there will be significant gross profitable licensing opportunities in the future. The era of indiscriminate content spending is over.

Furthermore, Q4 seriously impacts the investment thesis:

Management trust and competence

Size of the company & economies of scale

Company viability

Most importantly, this development has also damaged my trust in management. Previously, I gave management the benefit of the doubt based on the pedigree of John Hendricks, the Discovery Channel's founder and CURI's chairman. However, this quarter has revealed competence issues with the management of Curiosity Stream. As a reminder, content licensing was the most significant portion of their revenue in Q3 2022. In no previous disclosures, I saw that most of this had 0 gross margins. No wonder CURI was unprofitable. If management knew about this, this begs the question - why did they focus on growing this unprofitable portion of the business? Was it to raise money for the IPO? Was it to imply CURI was a company with a faster growth profile? Over the past few years, there has been much revenue growth in content licensing, while other revenue lines have grown much slower. Management claims to be long-term, but any reasonable person can tell that “investment” in these content assets is an unsustainable and unneeded cash burn. Previously, Clint was proud of his efforts to “diversify” revenue streams”. Now that easy money is gone and investors value profitable companies - management casually mentions that all this revenue is 0 gross margin. This is not how to build trust with investors; importantly, capital has already been wasted.

“The accounting treatment around our presales content licensing, as it’s existed for the last 18 months to 24 months, has been zero margin.” - Clint Stinchcomb, CEO, Q4 2022 Q&A

On the other hand, Q3 implied that licensing deals are “particularly” attractive.

“So returning to our revenues, content licensing was our most significant category this quarter, generating $10.8 million of revenue, an increase of 60% year-over-year. Notably, this quarter saw both what we refer to as presales and content library licensing transactions. Those library licensing deals tend to have particularly attractive margin characteristics.” - Peter Wesley, CFO, Q3 2022 Q&A

Furthermore, listening to the Q&A, Clint seemed to be excuse-making, rambling and unclear. He admits to being late for price increases and FAST. The company also didn’t release the subscriber number, which is suspicious. On the other hand, the CFO, Peter, spoke with more confidence and clarity. Speculating for a moment, I suspect Peter is the driving force for many of these efforts. He recently joined in May 2022. In conclusion, this quarter has made me lose trust in the management.

Secondly, with a lower revenue number, I’d argue CURI is potentially too small for me to invest in. Given this updated information, I’d be concerned about being invested in such a small company - revenue-wise. Companies have specific fixed costs - accounting, investor relations and HR. The original thesis expected that CURI would continue to grow revenue slowly. I was expecting about ~90M in revenue in 2022, and the top for 2023 is expected to be closer to half that at 45M; CURI would need to grow at a much faster growth rate to become profitable or, more likely, a much more extended period to reach profitability. The media industry is highly competitive - with more and more entertainment choices competing for our attention (with giants like Apple, Meta, Netflix, and Video Games).

Finally, all these new implications lead me to question the long-term viability of the business, with ~25% (19M) of the total revenue being presale 0 gross margin revenue. How much demand is there actually for a pure-play factual streaming service? If we remove pre-sales, we can see the growth rate was only 13% in 2021 and 48% during covid, much lower than the reported 79% growth rate achieved. If we project it to 2023, we see that CURI would have negative revenue growth.

On the bright side, there is still good growth for direct-to-consumer subscriptions.

Valuation

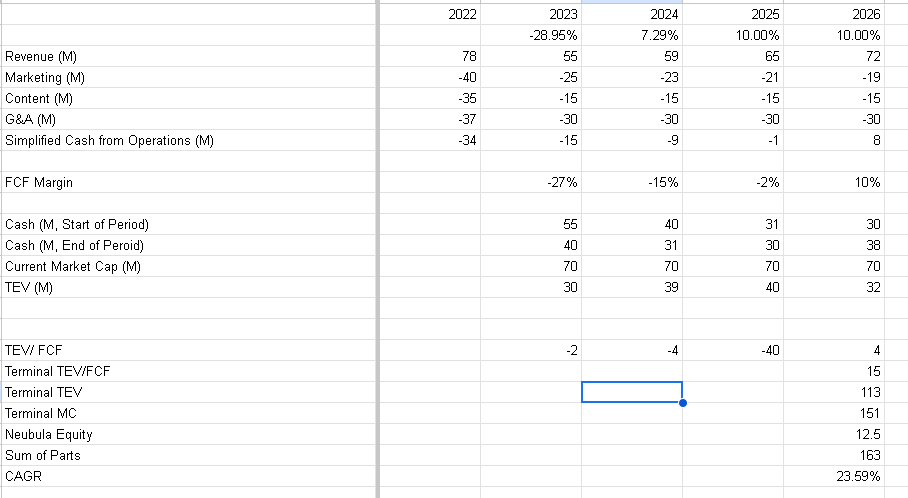

CURI is generally still on its path to profitability and is in the best position to achieve profitability as they have ripped off the band-aid this quarter. However, this has come at the cost of resetting the starting position. The 2023 guide is dire; Management has guided in 2023 a 20-25M marketing spend and 10-15 cash content spend. Suppose we annualise G&A of 7.6 in Q4 2022 and the teeny 11-13M revenue guide for Q1 2023 with some growth throughout the year. Notably, they have also walked back the positive FCF guidance in 2023. Management has guided (6)M - (8)M of negative free cash flow Q1 2023

Modelling meagre revenue growth of 7% in 2024 and recovery to 10% in 2025 and 2026. I model content spending and G&A as flat, as they need some content renewal to balance the churn of current users. Given CURI's leanness, I also model G&A as flat as cutting personnel will be challenging. The only place they can cut is Marketing, and I model a slight reduction in marketing.

I mainly looked at the balance sheet in my previous thesis since I assumed CURI was close to profitability. However, that thesis has been proven wrong, and I’m now modelling that CURI will only be cash neutral by 2025 and profitable by 2026 with a 10% FCF yield (similar to Netflix) instead of 2023. The management blindsided me and I should be more sceptical of the breakneck revenue growth from content licensing.

As a result, CURI will consume more cash, with around 38M in cash by 2026. From an acquirer's viewpoint, I would purchase the Video Assets & cash stream attached to that at 15x FCF (excluding cash) or a ~6.6% yield. This seems fair with 10-year treasuries at ~3.5% yield when writing. Adding back the cash would result in a 151M market cap for the CuriosityStream Business. Separately, I value Nebula stock at cost - 12.5M, although Nebula has been doing very well and might be worth more than CURI in the long term. This results in a Sum of Parts of ~163M by 2026. Suppose we compare it to the current market cap of ~70M at the time of writing. This represents ~132% upside in 4 years or 24% CAGR.

In other words, about a double in about 4 years.

Conclusion

If I were a Bull, I would focus on ripping the band-aid and its only upside from here. Plus, the management’s focus on reining in cash over superfluous metrics like revenue. I like the reduced emphasis on unprofitable partnerships and fostering direct customer relationships. I also like reducing content cash spend, raising prices, easing marketing and surprisingly cutting G&A. Lastly, the fact that CURI 0.00%↑ is already cheap and trading near cash.

On the other hand, if I was a bear. I would focus on the previous self-inflicted waste of marketing, content cost, management incompetence and the setback in revenue that is now revealed in the current quarter. The increase in time required to reach profitability and the risk attached to that.

CURI is still an acceptable investment if you can hold it for the next 3-4 years. However, given the difficulty of predicting the future over a long period, there is significantly more uncertainty than 90 days ago. Risk increases with that increase in time; many things can happen in 4 years, both negative consequences & potential upsides like Nebula. With the coming recession and other stocks at lower prices, as stated in the previous Q3 update, I do not think it is one of the better deals at the current prices. You can buy less risky large-cap stocks with similar return profiles or similar risk with better return profiles. Confidence and trust have been lost, and CURI is a much smaller company (revenue-wise) than 90 days ago, with a much longer time horizon to profitability. Weighing both sides of the argument, I’m overall neutral and rate CURI as a hold.